ARVAL 26 & BEYOND

Tax evolution for 2023

Arval Mobility Observatory

17 Feb 2023

As 2023 begins, Arval Mobility Observatory is pleased to share with you a synthesis of changes to statutory taxation and the associated mechanisms evolutions in Europe, by country. As follows, you will find a non-exhaustive list highlighting the evolution of Governmental taxation, grants and bonus schemes for 2023 in some European countries (such as Belgium, France, Germany, Italy, Greece, Luxemburg, the Netherlands, Norway, Portugal, Spain, Sweden, Slovakia) Switzerland and the United Kingdom.

Belgium

Social contribution (CO2-tax)

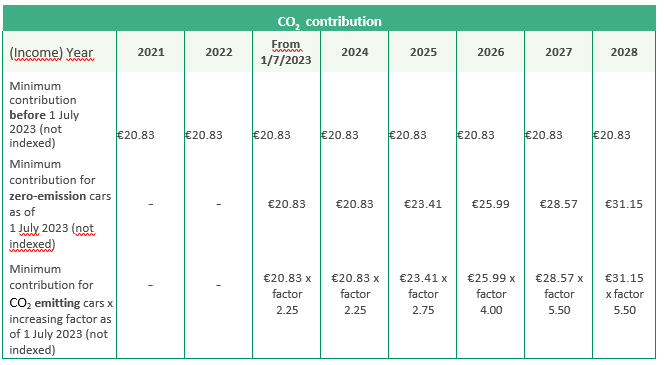

From the 1st of July 2023 onwards, the Belgian Government will gradually increase the social contribution that the buyer has to pay for cars emitting CO2.

In addition, the minimum contribution will also be increased in phases from 2025 onwards, reaching a minimum monthly contribution of € 31.15 (not indexed) in 2028. The current scheme will continue to be effective, but the result obtained under that scheme will be systematically multiplied for CO2 emitting vehicles by an increasing factor:

- Until the 31st of December 2024, this factor is 2.25

- In 2025, the factor will increase to 2.75

- In 2026, the factor is to be increased to 4.

- As of 2027, the factor will peak at 5.50.

Fiscal deduction of car costs

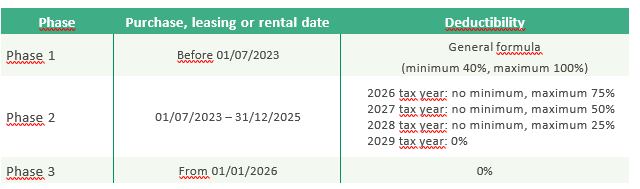

Plug-in hybrid electric cars purchased or leased from the 1st of January 2023 will see the fiscal deduction of petrol or diesel costs limited to a maximum of 50%.

Cars emitting CO2 emissions (including PHEVs) purchased/leased from the 1st of July 2023, will enter into a transitional taxation scheme. During this transitional period, the current scheme will continue to apply, but the deductibility caps will be systematically lowered from income year 2025 (tax year 2026) onwards, while the minimum deductibility percentage will no longer apply.

Additionally, the tax deductibility will be capped at 75% for tax year 2026, 50% for tax year 2027 and 25% for tax year 2028, finally leading to a full deduction ban for tax year 2029.

Vehicles for which no CO2emission data is available will not be eligible for a deduction.

BIK taxation 2023

For the 2023 income year (2024 tax year), the benefit in kind amounts to at least €1,540 per year, before deduction of any personal contribution.

France

Ecological bonus

The decrees n° 2022-960 and n°2022-1761, published in the Official Newspapers on the 30 of June and 30 of December 2022, are modifying the eligibility criteria of the ecological for the purchase or the lease (for contracts with a duration equal or superior to two years) of a private car or an LCV.

From the 1st of January 2023, Plug-in Hybrid Electric Vehicles (PHEV) will cease to be eligible for the ecological bonus of a 1 000 € regardless of the autonomy or their list price.

Only Battery Electric Vehicles (100% electricity powered) and Hydrogen Fuel Cell Vehicles (HFCVs) will be eligible for the bonus. The amount of the bonus is depending on the list price of the purchased/rented vehicle.

Recently, for the eligibility of electric private vehicles to the ecological bonus, a 2.4 tons weight limit has been established. For private vehicles which the price of is inferior to 47 000 €, the bonus for private individuals has been taken from 4 000 € in 2022, to 3 000 €.

In opposite to 2022, no bonus is to be granted for vehicles which the net list price of is sitting above 47 000 €.

For LCVs, the ecological bonus accorded to private individuals has been reduced to 4 000 € (from 5 000 € in 2022).

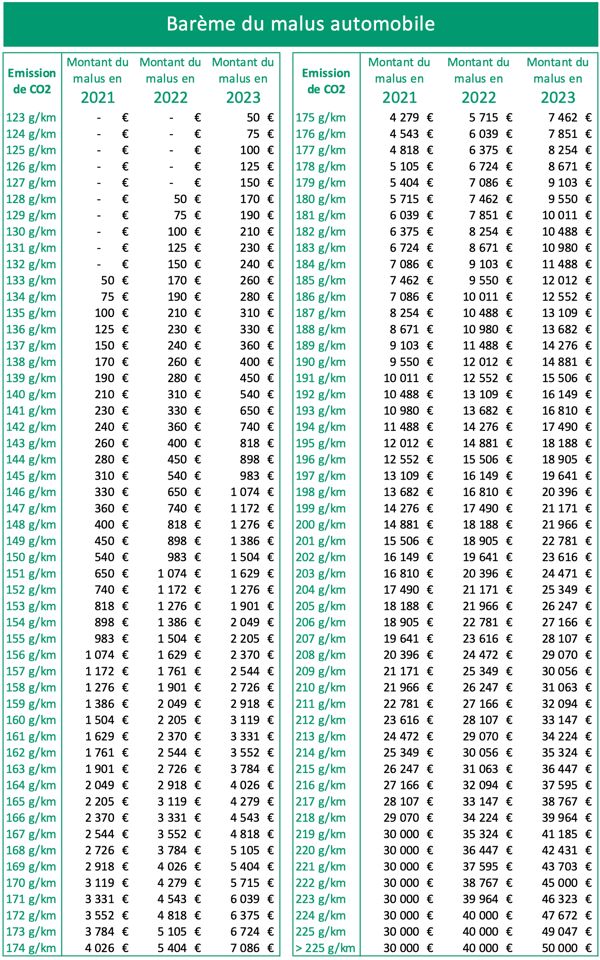

Ecological malus

As every year, the malus’ scale on CO2 emissions for tourism vehicles is becoming stricter; from the 1st of January 2023, it applies to every tourism vehicles which the CO2 emissions of are equal or superior to 123g, 5g less than last year. For 123 g of CO2, the tax starts at 50 €. The 1 000 € threshold is reached from 146 g (against 151 g in 2022).

The top threshold will be as high as 50 000 € for the vehicles having a CO2 rate higher than 225 g (against 40 000 € for 223 g in 2022).

BIK

The 8th of December 2022 Social Security’s official newsletter has established the prolongation for two years (until the 31st of December 2024) of companies’ BIK assessment for the provision of an EV and the use of a charging station.

For the calculation of social contribution, the advantage resulting from the provision of an EV to employees will not take into account the electricity fees engaged by the employer for the vehicle’s charge and will be systematically assessed after a 50% depression which the amount of is capped at 1 800 € per year.

Along the same period, the BIK resulting from the provision to employees of a charging station at the workplace will not be taken into account.

The full article is available here in French : La Fiscalité en 2023 | mobility-observatory.arval.fr

Germany

PHEV

The benefit in kind for Plug-in hybrid is 0.5% of the list price if the vehicle does not emit more than 50 grams of CO2 or can provide an electric range of at least 60 km. As of 2023, the German Government will no longer subsidize Plug-in hybrid vehicles' purchase or lease.

In addition but not yet announced: The halving of monetary benefits should only apply if the vehicle is mainly operated in purely electric drive mode. The minimum electric range of the cars is expected to be increased again to 80 kilometers from August 1, 2023. The measures announced by the federal Government have not yet been implemented due to the current delivery times. However, the announcements mean a certain degree of uncertainty with regards to the tax regulations applicable to the vehicle’s delivery.

BEV

The purchase or lease of fully electrified vehicles and fuel cell electric vehicles are subsidized on a staggered basis by the German Government:

- Net list price up to 40,000€: 4.500€

- Net list price between 40,000€ and 65,000€: 3,000€

The leasing period must be at least 24 months long to qualify for the full subsidy listed above and as of the 1st of September, only private individuals will be eligible to apply. From the moment the 3.4 € billion provided for 2023/2024 will have been distributed, the environmental bonus (Bafa) will expire immediately. On top of that, the leasing period must be at least 12 months long to qualify for the reduced subsidy. The benefit in kind for fully electrified vehicles and fuel cell electric vehicles is 0.25% of the list price with a gross list price below 60,000€ and 0.5% for vehicles with a gross list price over 60,000€.

From 1 September 2023, only private individuals can apply and receive the funding measures.

Another funding measure for fully electrified vehicles is the THG-Quote. The THG-Quote serves as a legal instrument to reduce CO2 emissions and achieve fuel companies' climate targets. From 2022, electric vehicles owners can benefit from this THG-Quote and earn money with their zero-emission cars by selling their vehicles’ saved CO2 emissions to companies that put fossil fuels on the market. Different providers in the market will handle this quota trading, and the payment will be made once a year per vehicle. In some cases, up to €400 can be earned annually with THG-Quote-trading. The emission savings depend on the vehicle class. Only a registration certificate is required to earn the money.

Greece

As of 2023, the Greek Government provides a 30% subsidy for the purchase of any Battery Electric Vehicle (BEV), up to a maximum of 8000€. Additionally, if the BEV buyer withdraws from circulation its old internal combustion engine vehicle, the maximum amount of the subsidy will be increased to 9000€. Moreover, BEVs are exempted from Road and Registration Tax and employees driving a BEV company car will also be exempted from paying BIK (Benefit In Kind), provided the vehicle purchase price before taxes does not exceed 40,000€. The amount above 40,000€ is subject to taxation.

For the purchase of a Wallbox, the Greek Government is providing a 500€ subsidy per Wallbox.

The Government has also announced a program to support the installation of public and private chargers, the details of which, will be known later this year.

On top of that, a 40% subsidy for electric motorcycles or minicars (categories L5e to L7e) has been established up to a maximum of 3000€. As such, the Government also unveiled a 40% subsidy up to a maximum of 800€ on electric bicycles.

Italy

PURCHASE VEHICLES INCENTIVES

- For the year 2023, the Italian Government has allocated funds to incentivise the purchase of new* low-emission vehicles, with the aim of renewing the vehicle fleet circulating in Italy and accelerating the energy transition [*the car must be new, i.e. registered for the first time in Italy, and Euro 6. Km0 cars, cars previously registered outside of Italy and used cars are excluded from this initiative].

- Overall, more than 575 € million were allocated based on following vehicle emissions scheme:

- 0-20 g/km (BEV): 190 € million (total for individuals + companies | only for PC | LCV excluded)

- 21-60 g/km (PHEV): 235 € million (total for individuals + companies | only for PC | LCV excluded)

- 61-135 g/km (FHEV-ICE): 150 € million (only for private individuals / only with scrapping)

- In line with last year, the Government bonus increases in relation to CO2 emission and car scrapping:

- 0-20 g/km: 3,000 € without scrapping; 5,000 € with scrapping; bonus for new cars with a list price (including accessories) up to 35,000 € (42,700 € including VAT)

- 21-60 g/km: 2,000 € without scrapping; 4,000 € with scrapping; bonus for cars with a list price (including accessories) up to 45,000 € (54,900 € including VAT)

- 61-135 g/km: no bonus without scrapping; 2,000 € with scrapping; bonus for cars with a list price (including accessories) up to 35,000 € (42,700 € including VAT)

- For Long Term Rental and car sharing companies the amount is 50% of that provided for Private Individuals:

- 0-20 g/km: 1,500 € (without scrapping); bonus for new cars with a list price (including accessories) up to 35,000 € VAT excluded (42,700 € including VAT)

- 21-60 g/km: 1,000 € (without scrapping); bonus for cars with a list price (including accessories) up to 45,000 € VAT excluded (54,900 € including VAT)

- In order to be eligible for the incentive, vehicles must be registered within 180 days from the date of booking the incentive. Beyond this time limit, the incentive will not be recognised.

- Scrapping (which concerns only Private individuals) is mandatory only for those who intend to purchase vehicles with emissions between 61-135 g/km. On the other hand, who opts for electric and plug-in cars can obtain an incentive even without scrapping an old car. The scrapped car must be in a class below Euro 5.

- The rule is that the car purchased with the incentive must be kept by the owner for a minimum number of months: Private individuals: at least 12 months; LTR companies: at least 12 months; Car Sharing Companies: 24 months

CHARGING POINTS INCENTIVES

- The Italian Government has also allocated EUR 40 million for the development of recharging infrastructures; the bonus is a contribution equal to 80% of the total spending (purchase and installation cost) of infrastructure. It consists of an immediate contribution, supported by the Ministry of Economic Development, and is dedicated for individuals (private houses and condominiums)

- The maximum contribution changes depending on whether the installation takes place in a private home or in a condominium building: 1,500 € per individual; 8,000 € in the case of installation in the common parts of a condominium building.

LOCAL CONCESSIONS

- In addition to 2023 Government incentives, a number of concessions for electric vehicles are extended at regional level and in some large metropolitan cities:

- Car tax exemption:

-

- Exemption for the first 5 years after registration; for the following years a tax of 25% of the amount for corresponding petrol/diesel vehicles

- Only for Valle D’Aosta - Exemption for the first 8 years after registration; for the following years a tax equal to 25% of the amount for the corresponding petrol/diesel vehicles

- Only for Lombardia and Piemonte - Permanent exemption

-

- Free access Low Emission Zone (e.g. Rome, Milan, Naples, Turin, Palermo, … )

- Free / discounted parking: (e.g. Rome, Milan, Naples, Palermo, …)

Luxemburg

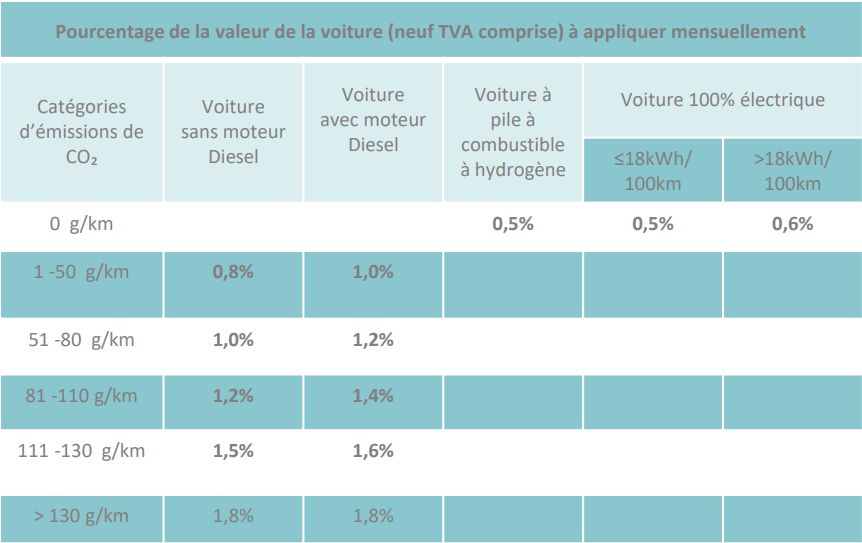

Following to the decision of the Ministry of Mobility and Public Works, the latest changes regarding benefit in kind (BIK) which will take effect from 01/01/2023 are as depicted below:

- CO2 emissions thresholds adjustment due to technological developments in vehicles

- BIK rate increase for electric vehicles with an energy consumption of more than 18 kWh/100 km; from 0.5% to 0.6%

- Change in the BIK for vehicles with internal combustion engines with CO2 emissions of more than 80 g/km.

All vehicles ordered in 2022 and delivered in 2022/2023 will be subject to the new rates. As such, all vehicles ordered in 2023 will be subject to this new rate.

Netherlands

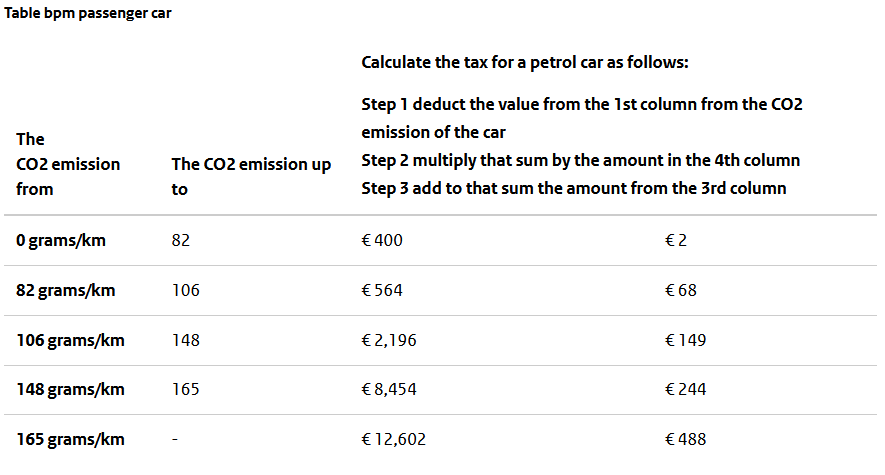

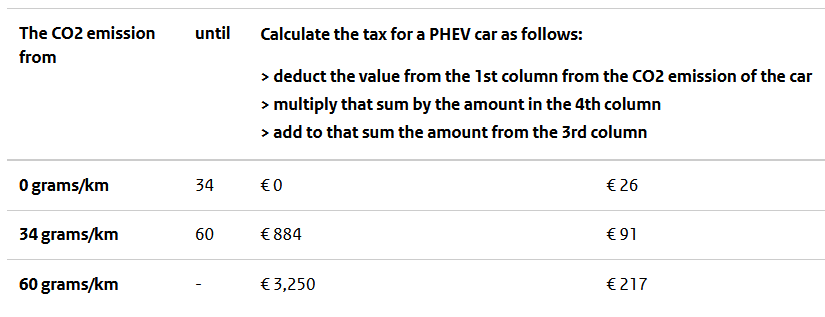

BPM tax

The BPM tax, which is the private motor vehicle and motorcycle tax, remains linked to CO² emissions and increases further. From 2022, the rate increases by 2.3% each year until 2025. How much BPM you have to pay depends on the category of your car and the BPM rate of this category.

Combustion engine

Is the CO2 emission of your passenger car with a diesel engine more than 73 gr/km? Then in addition to the outcome of the table above, you will pay a diesel surcharge of 94.30 € per gram of CO2 emissions above 73 g/km.

PHEVs

The calculation is the same as with a non-PHEV passenger car.

If the combustion engine is a diesel engine, the diesel surcharge also applies here.

For fully electric cars, the BPM tax exemption will continue to exist until 2024.

For a delivery van, camper van or motorcycle you pay BPM over the net list price. The net list price is the list price minus the VAT. The BPM is also payable on extra options; for a delivery van, camper van or motorcycle you also pay BPM over the following extras included in the net list price:

- Extra options

- Accessories

- Additional costs for special versions

BIK tax

If the private use of the company car exceeds 500km a year, 22% of the vehicle’s catalogue value will be considered part of the driver’s/user’s income. There is a discount on this standard 22% rate for fuel efficient cars: instead of 22%, a 16% car benefit charge is levied if the car is not emitting CO2 (zero emissions vehicle). The discount rate of 16% only applies to the first 30 000€ of the catalogue price. For an amount above 30 000€, the regular 22% applies. This threshold does not apply to hydrogen cars. If the private use of a company car is less than 500km a year, no car benefit is charged. Vehicles keep the tariff for a period that is the same as the standard lease period (calculated from the moment the vehicle is registered for the first time). The Ministry of Finance has set the standard lease period to 60 months.

Individuals with a BEV have a lower percentage of the list price added to their income when using their company car for personal use. For petrol cars, this is 22%. For BEVs, it increased from 4% in 2019, to 16% in 2022 and to 17% in 2025.

Untaxed allowances

The untaxed homework allowance will be €2.15 by 2023. From January the 1st 2023, the tax-free mileage allowance for travel expenses was increased from 0.19 € to 0.21 € per kilometer. And from January the 1st 2024, this will increase to 0.22 € per kilometer.

Norway

Benefit in kind taxation in 2023

The benefit subject to withholding tax related to private use of company car is calculated at: 30 percent of the car's purchase price* up to NOK 338,800 (EUR 31,840), and 20 percent of any excess list price.

*Purchase price = list price + winter tires and other equipment, but no discount and freight cost.

The rates for the benefit subject to withholding tax apply accordingly when assessed as a taxable benefit.

In the case of a company car scheme for a part of the income year, the benefit taxation will be a pro rata temporis of the number of whole and commenced months during which the car was available.

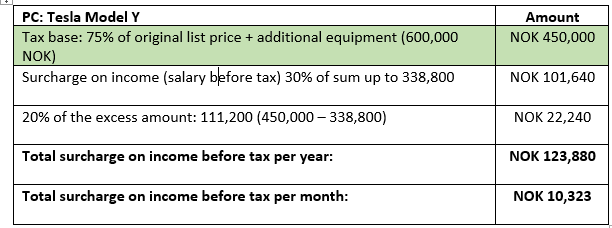

The basis for the calculation is normally a 100 percent of the car's list price as new, with some exceptions. The exceptions apply to both electric and thermal engine vehicles.

|

Exceptions: |

Calculation is based on: |

|

If the car is older than 3 years from as of the 1st of January of the income year |

75% of the vehicle's list price as new |

|

If you can document that the car used for work exceeds 40,000 km in the income year |

75% of the vehicle's list price as new |

|

In cases of combining:

|

56,25% of the vehicle's list price as new |

Removal of VAT exemption, introduction of a new weight fee

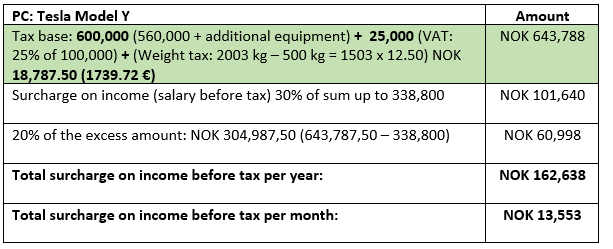

The discount for BEVs in company car taxation is removed. Electric cars are equated with traditional cars. In 2023, when purchasing a BEV, the VAT exemption will be removed for the amount of the purchase price that exceeds NOK 500,000. This means that only BEVs which costs less than NOK 500,000 will still have a full VAT exemption, until 2024 most likely.

Cars that are registered in 2023 will also get a new weight fee (NOK 12,5 per kilogram of the curb weight that exceeds 500 kilograms) added to the list price. In summary, benefit taxation will be calculated based on: List price + additional equipment + VAT (if purchase price exceeds NOK 500,000) + weight fee/one-time fee.

Example of calculation of benefit in kind of PC

Example of calculation of benefit in kind of Tesla Model Y Long Range, registered in 2023, with curb weight of 2003 kg and list price (importer's price) of NOK 560,000 + additional equipment (indicative prices excl. shipping) of NOK 40,000 , which equals to a purchase price of NOK 600,000, and no exemption benefits:

If the car is older than 3 years or can a work related driving document that exceeds 40,000 km in the income year, the car's list price is calculated as 75% of the car's original purchase price:

Benefit in kind for the use of LCV

If you have used your employer's LCVs for private travel, special rules apply for calculating the benefit. In this context, commercial vehicles mean vans class 2 and trucks with a total weight of less than 7,501 kg.

There are two different options for calculating the tax benefit of the private use of a commercial vehicle:

• The standard method: Tax based on the car's list price (with a base deduction from the list price)

• Kilometer rate: Taxes based on private use. Determined with an electronic vehicle logbook administered by the employer.

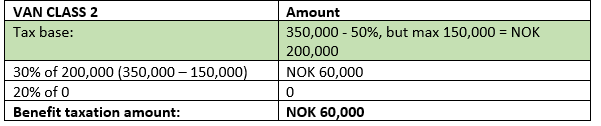

The standard method

The minimum deduction takes into account that commercial vehicles are less suitable for private use than ordinary company vehicles. Consequently, the list price is reduced by 50%, but up to a maximum amount of up to NOK 150,000.

Example: The commercial vehicle's new car price is NOK 350,000 :

No reduction is given for work related driving over 40,000 km on top of the minimum deduction.

Kilometer rate

For 2023, the rate for calculating the private benefit (based on actual use) is NOK 3.40 per km regardless of mileage.

Portugal

Autonomous taxation

Electric vehicles are now subject to “autonomous taxation” at a 10% rate, when the acquisition cost exceeds €62,500 (currently, charges are not subject to autonomous taxation).

Charges for plug-in hybrid and powered by CNG passenger cars (For CNG and LPG vehicles, the law is set for vehicles using exclusively this kind of energy. However the market offer is for Bi-fuel, thus LPG vehicles have no effective benefits), are now taxed at the same autonomous taxation rates: 2.5%, 7.5% and 15% (currently, plug-in hybrids subject to 5%, 10% and 17.5% and CNG subject to 7.5%, 15% and 27.5%).

The increase in tax rates by 10 percentage points, applicable to entities that calculate tax losses, is not applicable in the 2022 and 2023 tax periods, when:

- The taxable person has earned taxable income in one of the three previous tax periods

- The declarative delivery obligations of Modelo 22 and IES, relating to the two previous tax periods, have been fulfilled in a timely manner

- These correspond to the tax period of commencement of activity or to one of the following two periods.

Spain

Public transportation

The Spanish Government is intending to boost the public transportation usage during 2023 with the help of the following measures:

- Zero-fare public transport subscriptions for public operated train links on short journeys & 50% discounts on Avant services (mid/long distance journeys in trains at a speed up to 250km/h) for regular travelers.

- Free seasonal travel passes and multi-trip tickets for state-run buses from February till the end of the year.

- The Government will finance the reduction of 30% of the passes and multi-trip tickets for public transport in the regions where local entities raise the overall discount to 50%, between January 1 and June 30, 2023. Some of the regions, like Madrid, will offer a total discount of 60% for their users.

- Collective public transport will be free in the Canary Islands and the Balearic Islands for recurring users throughout 2023.

New package of grants for electromobility

- Extension until December 2023 of “Plan Moves III” with discounts up to 7000 for purchasing an EV.

- Second phase of “Moves Fleets” program with aids for EV’s acquisition by companies that want to renew their fleets with between from 25 to 500 vehicles. In Addition to acquire EVs, aids also could be granted in order to set up the recharging infrastructure as to obtain systems of fleet management and/or to train employees for assuring a good fleet transition towards electrification.

Sweden

Bonus & Malus:

- Bonus:

No environmental bonus on cars sold during 2023.

- Malus:

Increased road tax during the first 3 years:

-

- 107 SEK per gram carbon dioxide when emission is above 75 and up to 125 gram per kilometer.

- 132 SEK per gram carbon dioxide for emissions above 125 gram per kilometer

- In addition for all diesel vehicles a fixed fee of 250SEK/year

- In addition for all diesel vehicles a CO2based extra fee. The vehicles CO2 emission times 13,52.

- For all non-diesel vehicles with a CO2 emission between 0-75 gram a 360SEK/year road tax remains unchanged.

BIK

The subvention of the BIK value is based on a reduction of the new vehicle price which is one of the main components of the BIK formula. Subvention is split between 3 vehicle categories and provides a 50% reduction of the new vehicle price up to the maximum subvention limits:

- BEV and hydrogen cars: 350 000SEK

- PHEV: 140 000SEK

- GAS vehicles: 100 000SEK

Hence, if a newly purchased BEV’s price is 800 000SEK the reduced new vehicle price for the BIK formula is 450 000SEK

Slovakia

Highway stickers

From the 1st of January the price of highway stickers will increase by 20; from 50 EUR to 60 EUR.

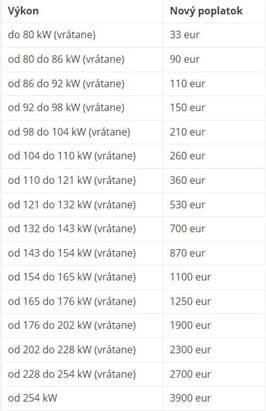

Registration fees

From April 2023, there will be an increase of the new registration fees of vehicles. It will take into account the ecological aspect. The new registration fee will be determined as the product of the vehicle's performance and ecological coefficient. The age of the vehicle will no longer be an important factor. The change will enable Slovakia, as in other EU member states, to increase the registration fee to motivate the purchase of ecological vehicles. New registration fee is listed below.

Car registration

From 2023 onwards, no de-registration fee will be charged and the pre-registration fee will be reduced by 50%, with a base fee; 33€. This rule applies also to EVs regardless of the age & power of its electric motor.

United Kingdom

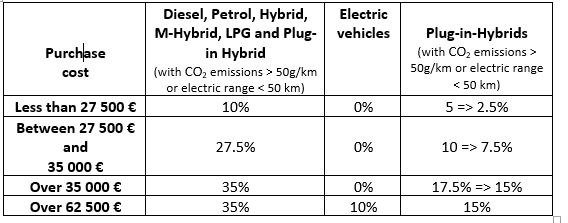

Three years of clarity on Company Car Tax rates (Benefit in Kind)

Support for electric and ultra-low emission cars emitting less than 75g of CO2 per kilometre has continued with the Government setting rates to April 2028, within the Autumn Finance Bill 2022. Currently rates are set at 2% for electric cars until 2024-25 and will then increase by 1 percentage point in 2025-26, a further 1% in 2026-27 and a further 1% in 2027-28, up to a maximum appropriate percentage of 5% for electric cars and 21% for ultra-low emission cars.

Rates for all other vehicles’ bands will be increased by 1 percentage point for 2025-26, up to a maximum appropriate percentage of 37% and will then be fixed in 2026-27 and 2027-28.

Vehicle Excise Duty unraveled for electric vehicles and vans

From April 2025, electric cars, vans and motorcycles will begin to pay VED in the same way as petrol and diesel vehicles. The Government has highlighted that this will ensure that all road users begin to pay a fair tax contribution as the take up of electric vehicles continues to accelerate. It will legislate for this measure in the Autumn Finance Bill 2022.

This means:

• new zero emission cars registered on or after 1 April 2025 will be liable to pay the lowest first year rate of VED (which applies to vehicles with CO2 emissions 1 to 50g/km), currently £10 a year. From the second year of registration onwards, they will move to the standard rate, currently £165 a year

• zero emission cars first registered between 1 April 2017 and 31 March 2025 will also pay the standard rate

• the Expensive Car Supplement exemption for electric vehicles is due to end in 2025. New zero emission cars registered on or after 1 April 2025 will therefore be liable for the expensive car supplement. The Expensive Car Supplement currently applies to cars with a list price exceeding £40,000 for 5 years

• zero and low emission cars first registered between 1 March 2001 and 30 March 2017 currently in Band A will move to the Band B rate, currently £20 a year

• zero emission vans will move to the rate for petrol and diesel light goods vehicles, currently £290 a year for most vans

• rates for Alternative Fuel Vehicles (for example hydrogen) and hybrids will also be equalised.

Van Benefit Charge and Car & Van Fuel Benefit Charges

From 6 April 2023, Car and Van Fuel Benefit Charges and van benefit charge will increase in line with the Consumer Price Index. The Government planned to legislate by way of Regulations in December 2022.

Van Benefit Charge and Car & Van Fuel Benefit Charges

From 6 April 2023, Car and Van Fuel Benefit Charges and van benefit charge will increase in line with CPI. The Government will legislate by way of Regulations in December 2022.

First Year Allowance for Electric Vehicle Chargepoints

The Government will legislate in the Spring Finance Bill 2023 to extend the 100% First Year

Allowance for electric vehicle chargepoints to 31 March 2025 for corporation tax purposes and 5 April 2025 for income tax purposes. This will ensure that the tax system continues to incentivise business investment in charging infrastructure.

Plug-in Car Grant removal:

On the 14th of June 2022, the Office for Zero Emission Vehicles (OZEV) removed the Plug-in Car Grant (PiCG) to new orders.

The £300 million grant funding will now be refocused towards infrastructure and extending Plug-in grants to boost sales of plug-in taxis, vans, trucks, motorcycles and wheelchair accessible vehicles, as announced in autumn statement.

Plug in Van Grant:

The Government extended its support for electric van; The Plug in Van Grant availability has been extended for an additional two years, to2024/5.

More detail on the Advisory Electric Rates

HMRC has provided more information on Advisory Fuel and Electric rates on gov.uk here - the new 8p per mile EV rate will be reviewed on a quarterly basis and will apply from 1 December 2022.