ARVAL 26 & BEYOND

Corporate Electrification Strategies in Europe: Resilient Overall, Uneven Across Markets

Arval Mobility Observatory

31 Mar 2026

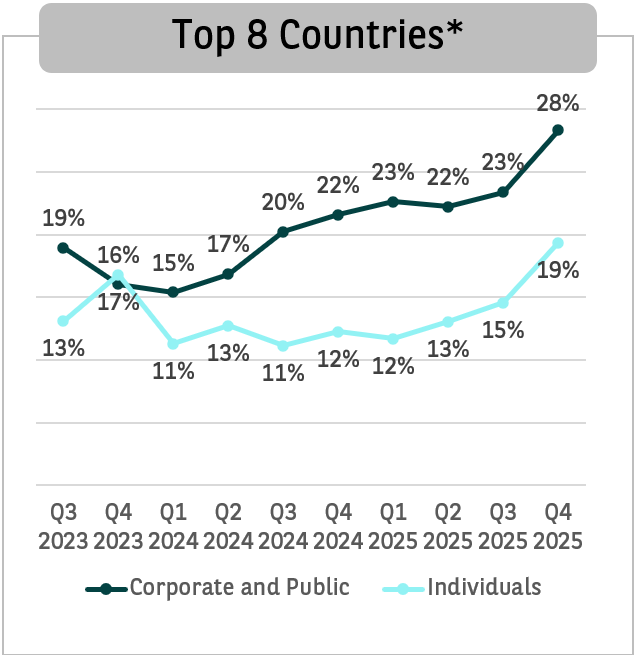

Across Europe’s largest registration markets, corporate fleets continue to lead BEV penetration, even if some countries experienced short-term slowdowns linked to regulatory and policy uncertainty. In Q4 2025, BEVs accounted for 28.3% of corporate passenger car registrations across the Top 8 countries * in Europe (including the UK) and 19.4% for individuals.

Corporate fleets’ stronger BEV penetration largely reflects the progressive adaptation of corporate car policies. BEVs are increasingly positioned as the default or preferred choice for company car drivers, as observed in the the Arval Mobility Observatory Barometer 2026

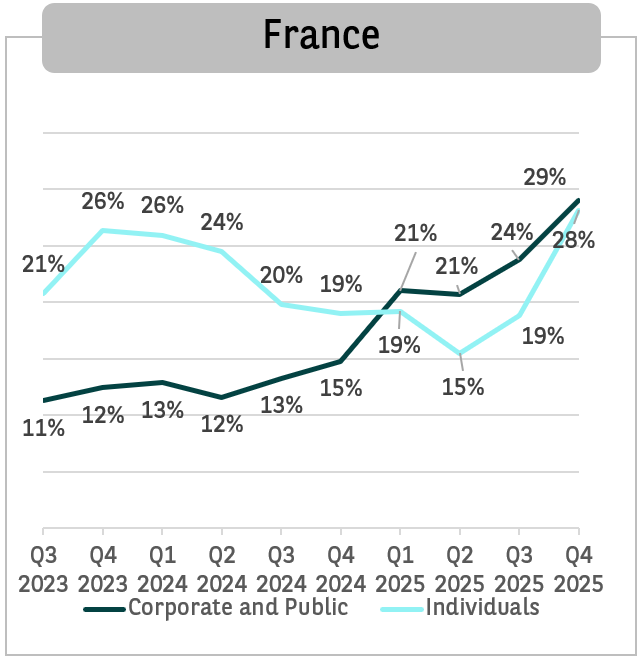

Fiscal incentives specifically designed for company cars continue to reinforce this dynamic. Notably, the higher BEV penetration among corporates is also observed in countries where private buyers benefit from purchase incentives, such as France.

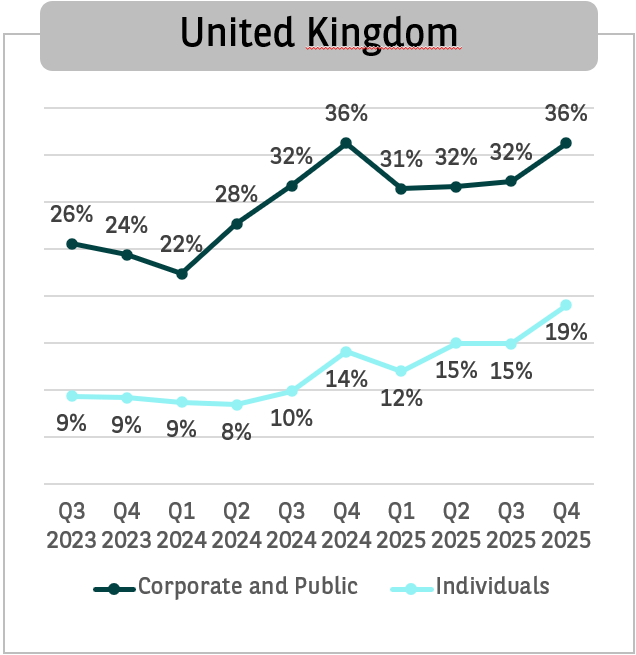

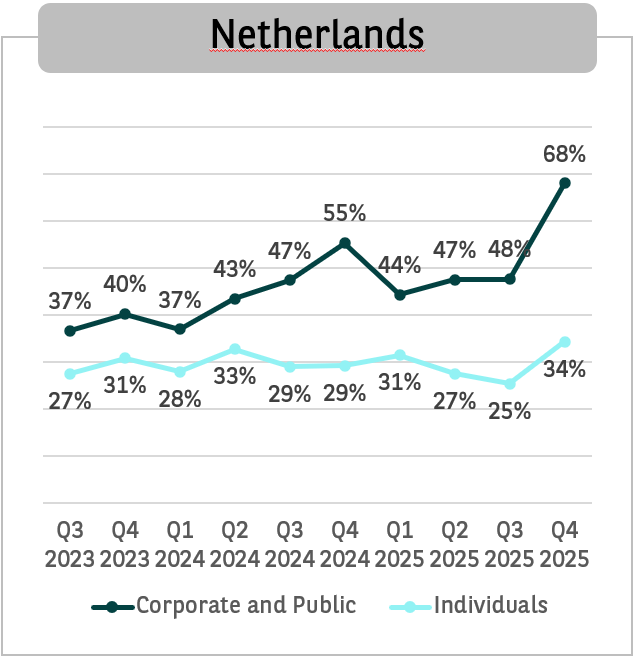

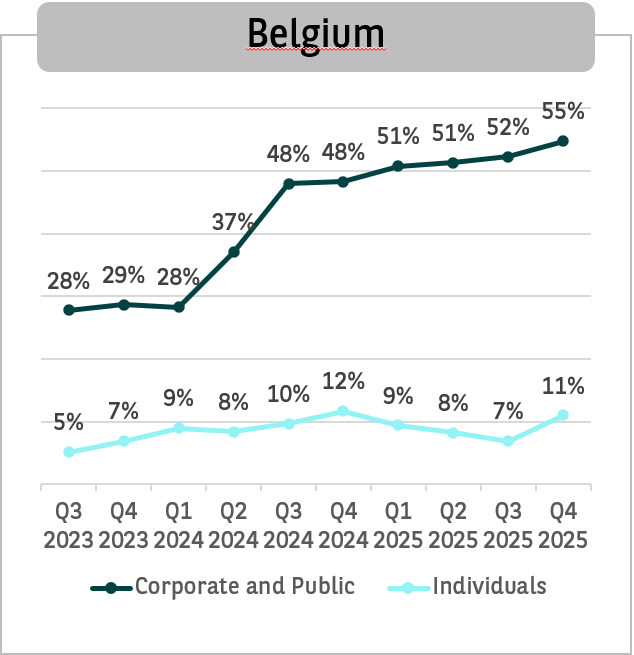

The gap between corporate and individual BEV adoption is particularly pronounced in Belgium, the Netherlands and the United Kingdom, where taxation that benefit fleets and company car create a strong and persistent advantage for corporate electrification. In France, BEV penetration among private individuals has also increased sharply in 2025, largely driven by the rollout of social leasing schemes, narrowing the gap with corporate fleets.

Quarterly BEV penetration in new Passenger Cars registrations – Top 8 countries*

*Top 8 countries in terms of registrations (around 80% of the market in Europe): Belgium, France, Germany, Italy, the Netherlands, United Kingdom, Spain and Poland. Corporates market data: share of BEV in total registrations of passenger cars for Corporates; Individuals market data: share of BEV in total registrations of passenger cars for Individuals, source S&P Global Mobility.

Market Context

After a decline in 2024, BEV registrations in Europe resumed growth in 2025, reaching 1.88m new passenger cars. While list prices remain higher than their ICE equivalent, lower running and maintenance costs continue to improve BEV Total Cost of Ownership.

However, the long-term sustainability of this advantage will increasingly depend on the stabilisation of residual values, as faster depreciation of BEVs still jeopardize the offer of affordable EVs.

Future growth of fleet electrification in Europe will continue to depend on a combination of European regulations (such as CAFE norms or the European Automotive Package) and national tax frameworks, which play a decisive role in shaping both corporate and private demand.

Corporate Fleets as a Key Driver of Electrification, amid Market Disparities

Corporate fleets continue to play a leading role in Europe’s electrification, not only because of fiscal incentives, but also due to long-term sustainability commitments and clearly defined car policies.

Although BEVs are increasingly competitive in TCO terms, private consumers generally remain more sensitive to upfront prices, whereas corporates base decisions on total cost considerations.

Netherlands

In Q4 2025, BEVs represented 68% of corporate passenger car registrations, compared with 34% among private users, making the Netherlands one of the most advanced large European markets in terms of corporate electrification. BEV penetration among private individuals also increased markedly in 2025, supported notably by a combination of relatively mature charging infrastructure, and sustained policy support over time.

Italy

Italy stands out as a unique case where BEV penetration among private individuals overtook corporates from Q4 2025. This can be explained by the strong impact of incentives targeting private users.

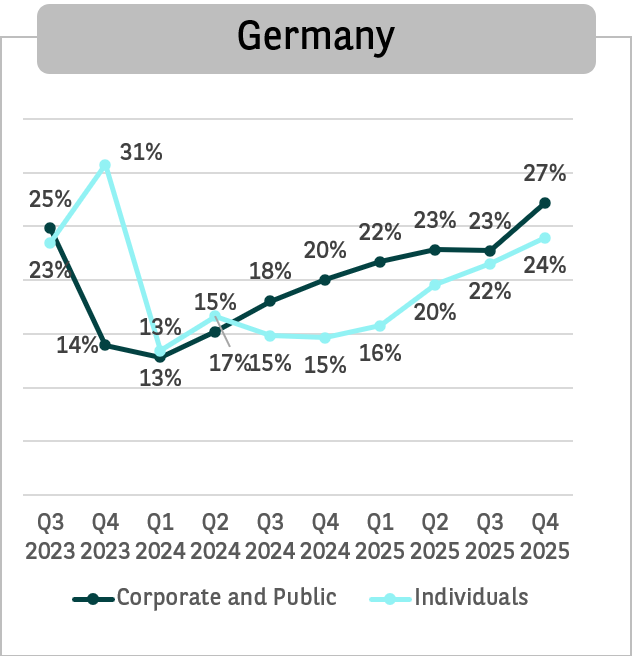

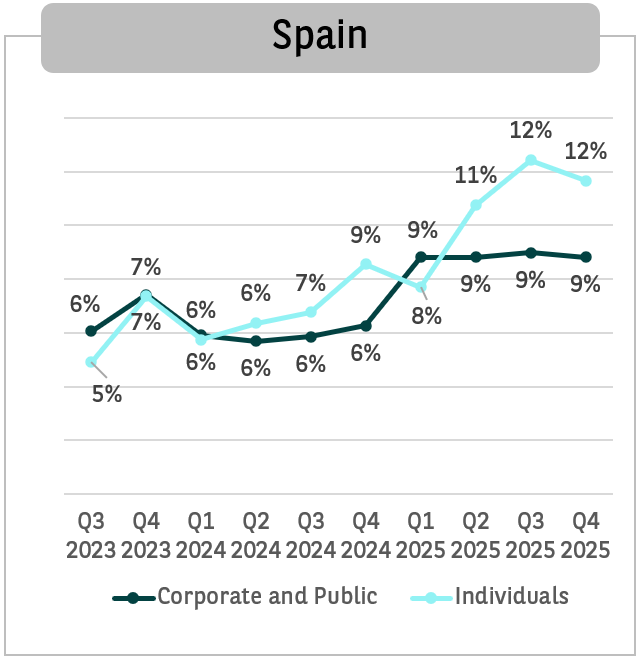

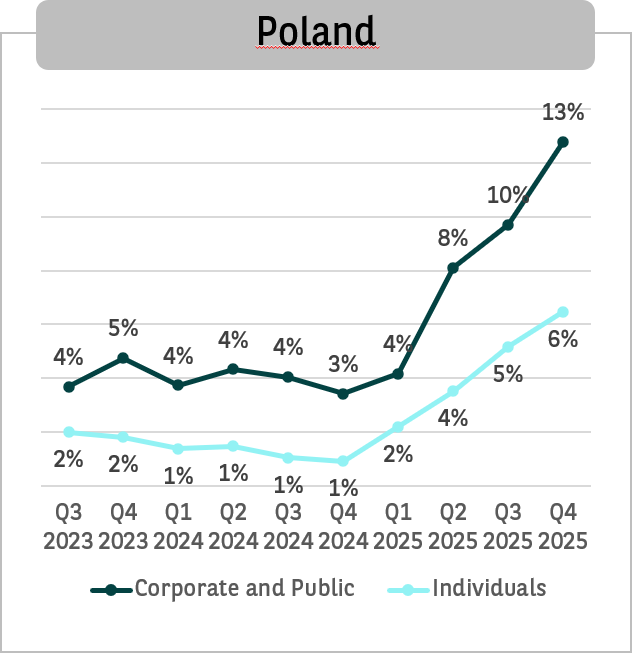

Quarterly BEV penetration based on registrations of Passenger Car - Details per country

Data is subject to change on a regular basis. For accuracy and reliability, users should always refer to the most recent official publications and updates before making decisions or drawing conclusions

S&P Data or Charts shall never be incorporated into a registration statement, securities related filing, prospectus, public or private debt issue documentation, any bond issue documentation or other offering document. S&P Data are provided by S&P "as is".