ARVAL 26 & BEYOND

The Arval Mobility Observatory's Global Fleet and Mobility Barometer 2026

Arval Mobility Observatory

19 Mar 2026

Arval Mobility Observatory’s fleet and mobility barometer 2026 finds companies moving from vision to action across electrification, TCO and workforce mobility

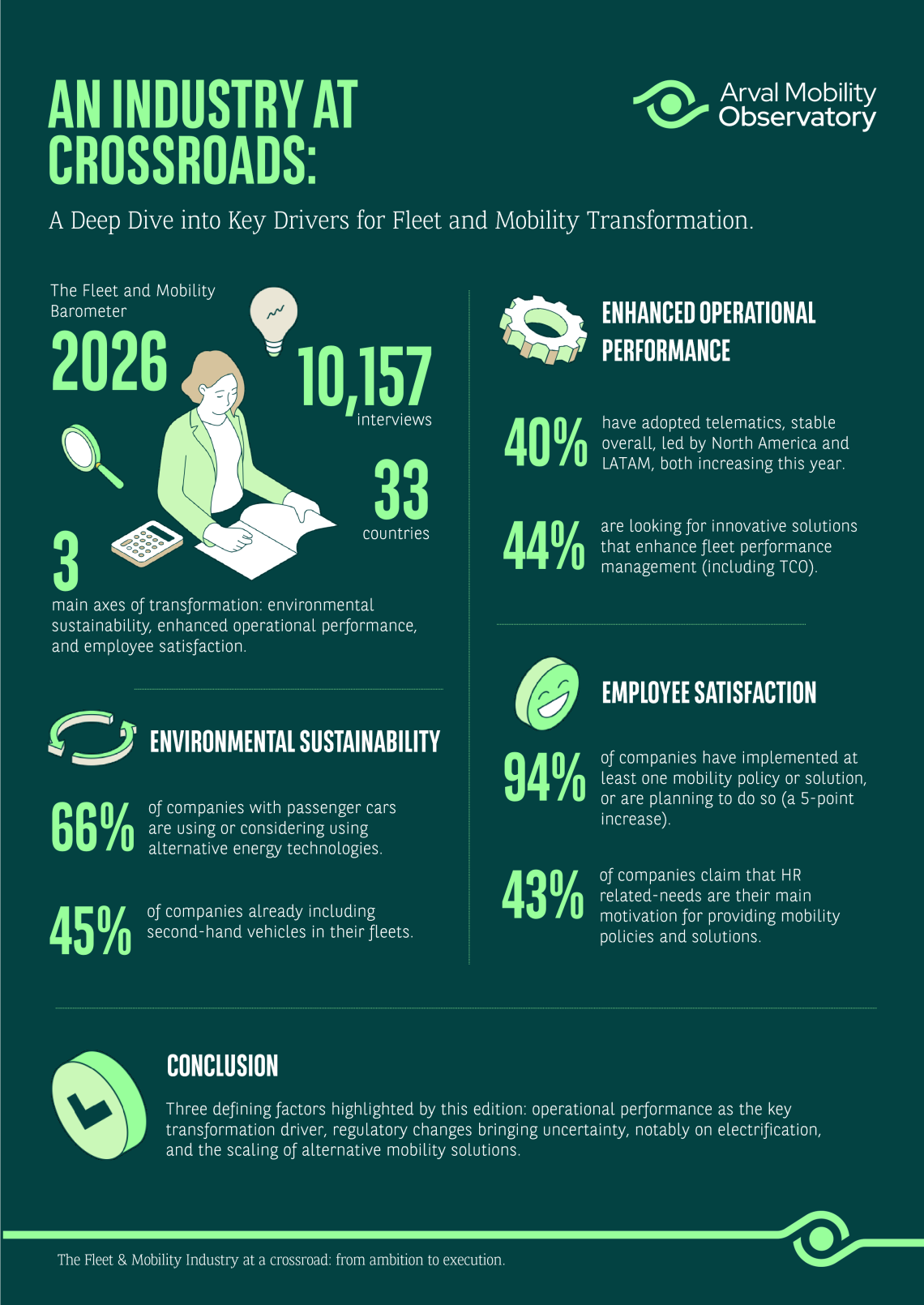

Arval, a BNP Paribas company and a global leader in full-service leasing and mobility solutions, unveils the 2026 Global Fleet and Mobility Barometer conducted by the Arval Mobility Observatory. Based on 10,157 interviews with fleet decision-makers across 33 countries, this new edition highlights a decisive transition: companies are moving from ambition to execution, redefining their electrification, cost-management and mobility strategies with a sharper operational focus.

Electrification: from ambition to operational execution

Electrification continues to anchor corporate fleet strategies, reflecting both environmental ambitions and long-term planning. This year’s Barometer confirms that a large majority of companies have firmly integrated alternative energy into their roadmap: 66% consider it a strategic priority, and 46% already operate electrified technologies, demonstrating that the transition is tangible and well underway. Europe, in comparison with North America and Asia-Pacific, remains the most advanced region, with 57% of organisations already using electric vehicles, and globally 66% report they already use or plan to deploy EVs within the next three years.

Overall, companies surveyed expect their electrified fleets to keep progressing, targeting within three years a mix of 33% BEVs, 36% PHEVs and 38% HEVs, confirming stable yet resilient ambitions for the energy transition.

Yet, as adoption accelerates, practical barriers weigh increasingly heavily on fleet decisions. The lack of adequate charging infrastructure remains the number one obstacle, cited by 68% of companies for passenger cars and 67% for light commercial vehicles. Beyond infrastructure, higher purchase prices for EVs and limited model availability continue to slow down certain segments, reminding decision-makers that ambitions must coexist with operational feasibility.

Despite these challenges, companies are taking a more structured approach to charging strategies, recognising them as a critical enabler of fleet electrification. Nearly all respondents have already implemented or plan to implement a dedicated charging policy1. More than half (56%) either operate or are preparing onsite charging capabilities, 67% are turning to public charging networks, and 21% now offer home-charging options, demonstrating a multi-pillars response to infrastructure gaps.

Regulatory pressure, including emerging initiatives remains influential but is no longer the only driver. In Europe, 48% of surveyed companies say they would take all necessary measures to comply with a hypothetical 100% EV requirement by 2030, while 46% state they would look for alternative mobility solutions if full electrification proves too restrictive, highlighting an increasingly nuanced approach to compliance and operational flexibility.

Cost control and predictive capabilities take centre stage

As electrification scales up and mobility offerings diversify, companies are placing a renewed emphasis on cost discipline and predictability. Managing Total Cost of Ownership (TCO) has surged to one of the top fleet leaders’ concerns: 31% identify it as one of their top three challenges for the next three years, a figure that rises sharply in certain regions, reaching 45% in North America and 40% in Asia-Pacific.

To navigate this evolving environment, organisations are turning to smarter, more connected tools that allow them to better anticipate issues, streamline operations and optimise expenses. Demand is rising for automated vehicle monitoring, predictive maintenance, and real-time visibility across vehicles, drivers, routes and deliveries. Integrated fleet management platforms, bringing together sustainability metrics, cost analysis and mobility insights, are becoming essential, signalling a shift toward comprehensive digital ecosystems capable of supporting complex, multilayered fleet strategies.

This evolution marks a turning point: companies are no longer simply seeking technological add-ons, but rather robust end-to-end systems that can reduce risks, improve performance and guide strategic decisions in an environment where both regulatory and economic pressures are intensifying.

Employee mobility accelerates and diversifies

Beyond vehicles and charging infrastructure, the Barometer highlights a profound transformation in employee mobility. In 2026, companies are not only expanding the number of solutions available to employees but are also reshaping mobility as a central component of their HR and sustainability strategies. A striking 94% of organisations worldwide have already implemented or plan to introduce at least one mobility solution, an increase of five points compared with 2025. Motivations are increasingly evident, with 43% citing HR drivers behind these initiatives, such as attracting talent, improving wellbeing and supporting hybrid work models.

Among the solutions gaining traction, car-sharing and car-pooling each attract 26% of respondents, while mobility budgets reach 30% adoption. Private lease and salary-sacrifice schemes (25%), as well as reimbursement options for personal vehicle or public transport use, further reflect a change toward more personalised, flexible and sustainable mobility offerings. This diversification confirms that employee mobility is now seen as a strategic asset, enabling companies to balance operational needs, environmental commitments and workforce expectations.

A sector entering a new phase

Compared with 2025, when electrification ambitions surged and many organisations set bold targets, the 2026 edition of the Barometer underscores a more grounded, execution-oriented phase. Operational performance is becoming a decisive differentiator, regulatory frameworks continue to evolve and influence decision-making, and alternative mobility solutions have become standard practice across most countries surveyed.

“The 2026 edition of the Fleet and Mobility Barometer clearly shows that companies have moved beyond the phase of defining their ambitions. This year, we observe a marked shift toward pragmatism: organisations are carefully balancing environmental goals with cost discipline, infrastructure constraints and the need for smarter digital tools. The Barometer highlights strong momentum, as well as a growing demand for predictability and for integrated digital ecosystems to ensure these strategies are implemented efficiently, sustainably and at scale”, says Dan Boiangiu, Director of Arval Consulting and Arval Mobility Observatory.

“The addition of Asia-Pacific to this year’s Barometer delivers a more comprehensive and contrasted global picture. Its fast‑advancing electrification and strong digital uptake enrich the established maturity of Europe and North America. Together, these perspectives reveal a universal shift from ambition to execution—though the pace and conditions vary widely across markets”, adds Caroline Pelissier, Head of Arval Mobility Observatory.

Methodology

The survey was conducted by independent research firm Ipsos between August 25 and November 12, 2025, through 10,157 interviews with fleet decision-makers across 33 countries. Respondents represented companies operating at least one vehicle, from SMEs to large corporates.

1 This result is calculated on all companies with at least one professional vehicle, which explains why it may exceed the share already using electric vehicles