ARVAL 26 & BEYOND

BEV penetration Q1 2026: how policy, market maturity and incentives shape adoption across Europe

Arval Mobility Observatory

16 Jun 2026

Disclaimer: The analysis presented in this article reflects market dynamics observed in Q1 2026. Since then, geopolitical developments — notably rising tensions in Iran — have begun to affect fuel prices. These impacts are not yet visible in the data presented here and are expected to emerge in subsequent quarters, notably from Q2 2026 onwards.

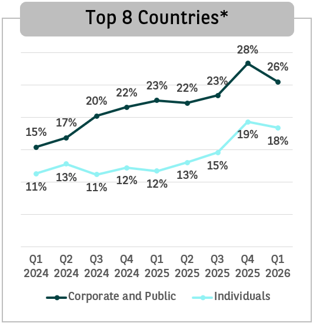

At the start of 2026, battery‑electric vehicles (BEV) continued to gain ground across Europe as they accounted for close to one in five new registrations.

A closer look at Q1 2026 tells a more complex story though: BEV adoption is still moving forward, but it is not following a single, linear path.

Q1 2026 figures showed that BEV adoption was still shaped by policy frameworks, incentives design and market maturity.

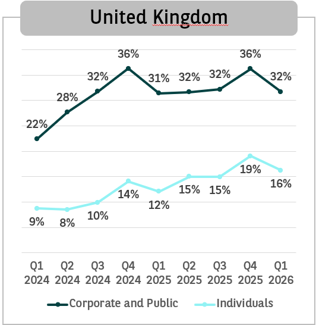

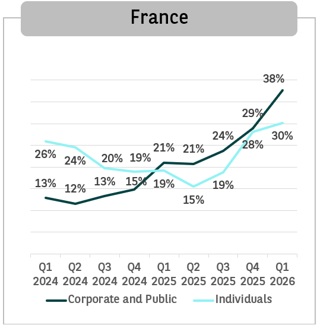

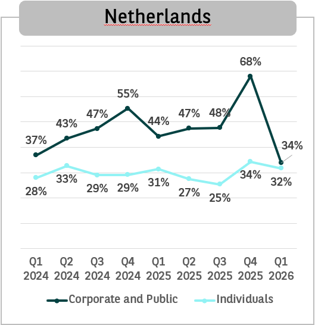

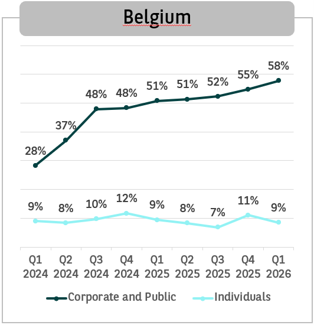

Markets such as France and Belgium continued to show strong BEV penetration, largely supported by stable company‑car taxation and well‑established fleet electrification strategies. Elsewhere, adjustments to fiscal frameworks have translated into visible quarter‑to‑quarter volatility. As seen in the Netherlands, BEV penetration experienced a sharp drop at the start of 2026 following a peak at the end of 2025. This pattern reflects strong policy timing effects, as upcoming fiscal changes led to a pull-forward of registrations into late 2025. As a result, part of the demand that would normally have occurred in early 2026 was brought forward, mechanically lowering penetration levels at the start of the year.

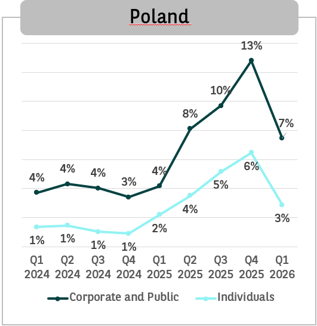

In Poland, the sharp drop in BEV penetration in Q1 2026 mainly reflects the end of the “NaszEauto” subsidy scheme, which had mechanically boosted registrations at the end of 2025. It was amplified by new fiscal rules introduced in January 2026, leading to a temporary pause in corporate purchasing decisions

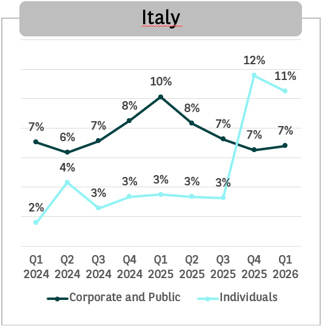

In Italy, corporate BEV registrations in 2025 and Q1 2026 remains low and has even slightly decreased due to the absence of concrete incentives for companies. On the other hand, BEV registrations by individuals made good progress as from Q3 2025 and renewed in 2026 due to the implementation of bonuses granted to individuals (not made available for corporates) for the purchase of EVs.

Quarterly BEV penetration in new Passenger Cars registrations – Top 8 countries*

*Top 8 countries in terms of registrations (around 80% of the market in Europe): Belgium, France, Germany, Italy, the Netherlands, United Kingdom, Spain and Poland.

Fleets still lead the race to electrification

Corporate fleets continue to account for a large share of BEV registrations across Europe. Their role remains central, particularly where electrification has become embedded in company car policies.

This pattern reflects a strategic shift: organizations are leveraging BEVs to meet decarbonization targets, and in the most advanced European countries, special incentives for low carbon cars are helping make this easier.

In addition, while the list prices of BEVs remain higher than prices of ICEs, their lower running and maintenance costs are shifting the balance of the Total Cost of Ownership - for Corporates - in the benefit of full electric passenger cars compared to fuel or petrol cars.

Private adoption: steady, but still cautious

Among private buyers, Q1 2026 confirms gradual progress rather than acceleration.

BEV penetration continues to rise, supported by incentives and a broader product offering. However, adoption remains uneven and closely tied to affordability and policy support, with hybrids often retaining a strong appeal.

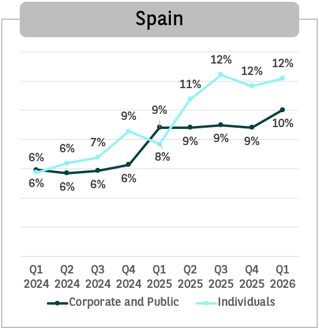

In Spain for example, BEV adoption is supported by strong and simpleincentives for individuals, including direct subsidies and tax benefits that significantly lower the cost of buying a car . Lower electricity prices and easier access to home charging also make electric vehicles more attractive. At the same time, limited support for corporates means that adoption is growing faster among private individuals. r

Quarterly BEV penetration based on registrations of Passenger Cars - Details per country

Graphs based on data from S&P Global Mobility, April 2026 - Corporates and individuals market data: share of BEV in total registrations of passenger cars for Corporates and individuals.S&P Data or Charts shall never be incorporated into a registration statement, securities related filing, prospectus, public or private debt issue documentation, any bond issue documentation or other offering document. S&P Data are provided by S&P "as is".